Cash, contactless, or QR code? With so many ways for shoppers to pay, it’s never been more important for small businesses to know what customers really want.

To find out what’s happening on the high street and online, we surveyed 2,000 UK consumers to see how they prefer to pay, why they choose those methods, and what’s changed since our last study in 2023.

Whether you run a market stall, café, or online business, our insights will teach you everything you need to keep up with customer expectations.

Our key findings

- 54% of UK shoppers say contactless is their favourite way to pay in-store — up 14% since 2023.

- Over half of Brits (56%) still carry cash.

- Cash use in-store is up 26%, since 2023, overtaking mobile wallets as the second most popular in-store payment method.

- Almost two-thirds (62%) prefer debit or credit cards for online shopping over alternative payment methods

- 45% have abandoned an in-store purchase because the payment system was down.

- Among 18–24s, mobile wallets are now more popular online than traditional card payments.

- Just over half (52%) feel comfortable using Open Banking, and 67% are open to biometric payments for extra security.

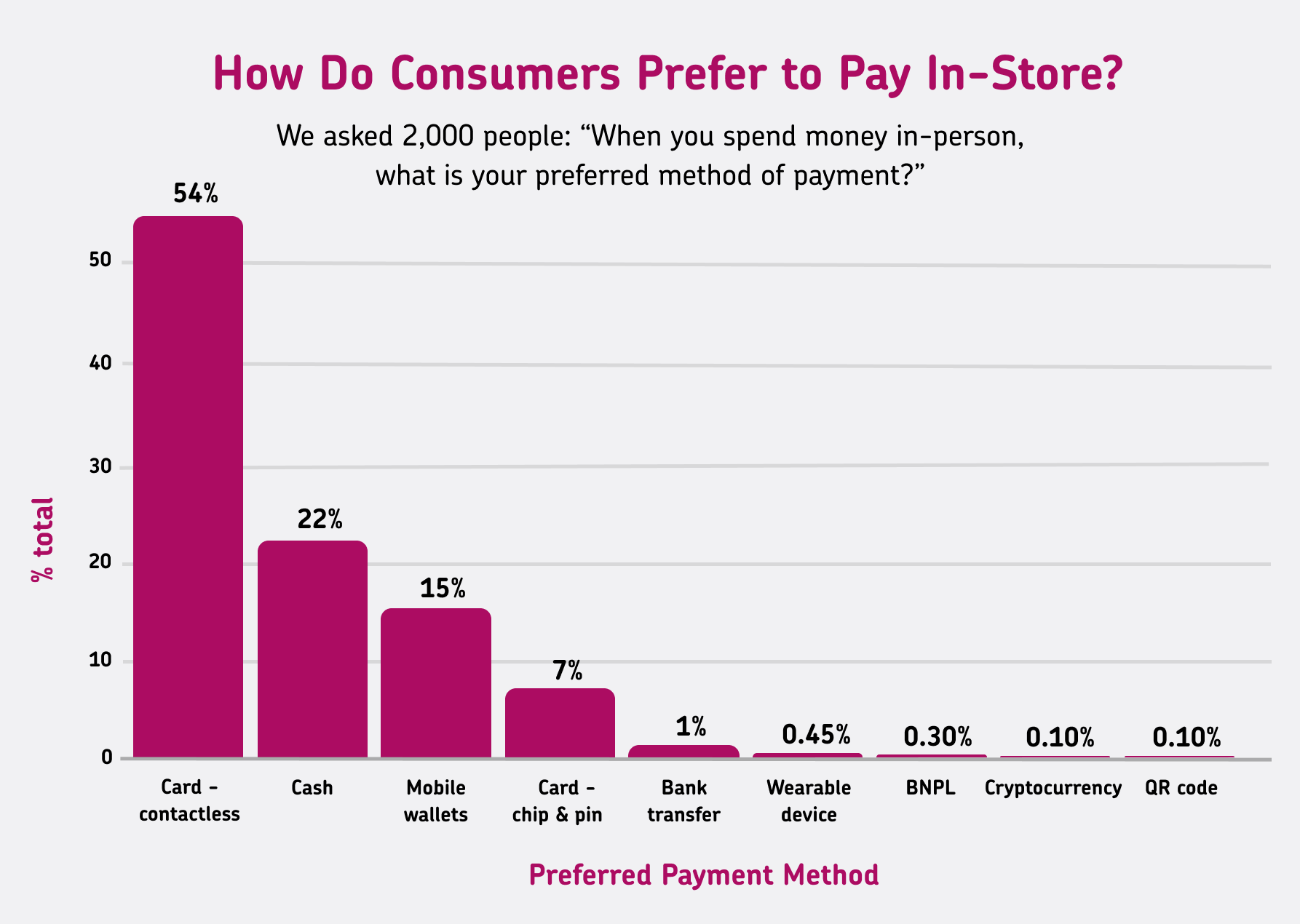

How do consumers prefer to pay in-store?

When it comes to paying in person, contactless remains the UK’s firm favourite, with over half (54%) of shoppers saying it’s their top choice at the checkout. It’s clear that speed and ease matter more than ever to today’s customers.

But it’s not all about tapping and going. One in five shoppers (22%) say they prefer to pay with notes and coins. Mobile wallets came in third (15%), while chip and PIN was chosen by just 7% of people.

So what’s driving these choices?

For most people, it’s all about ease. Four in five shoppers (79%) say they chose their payment method because it’s convenient.

Fast transactions and wide acceptance come next, at 42% and 28%, respectively, while only one in five (21%) said they chose their preferred payment method because it feels most secure, suggesting that many shoppers value speed over safety concerns.

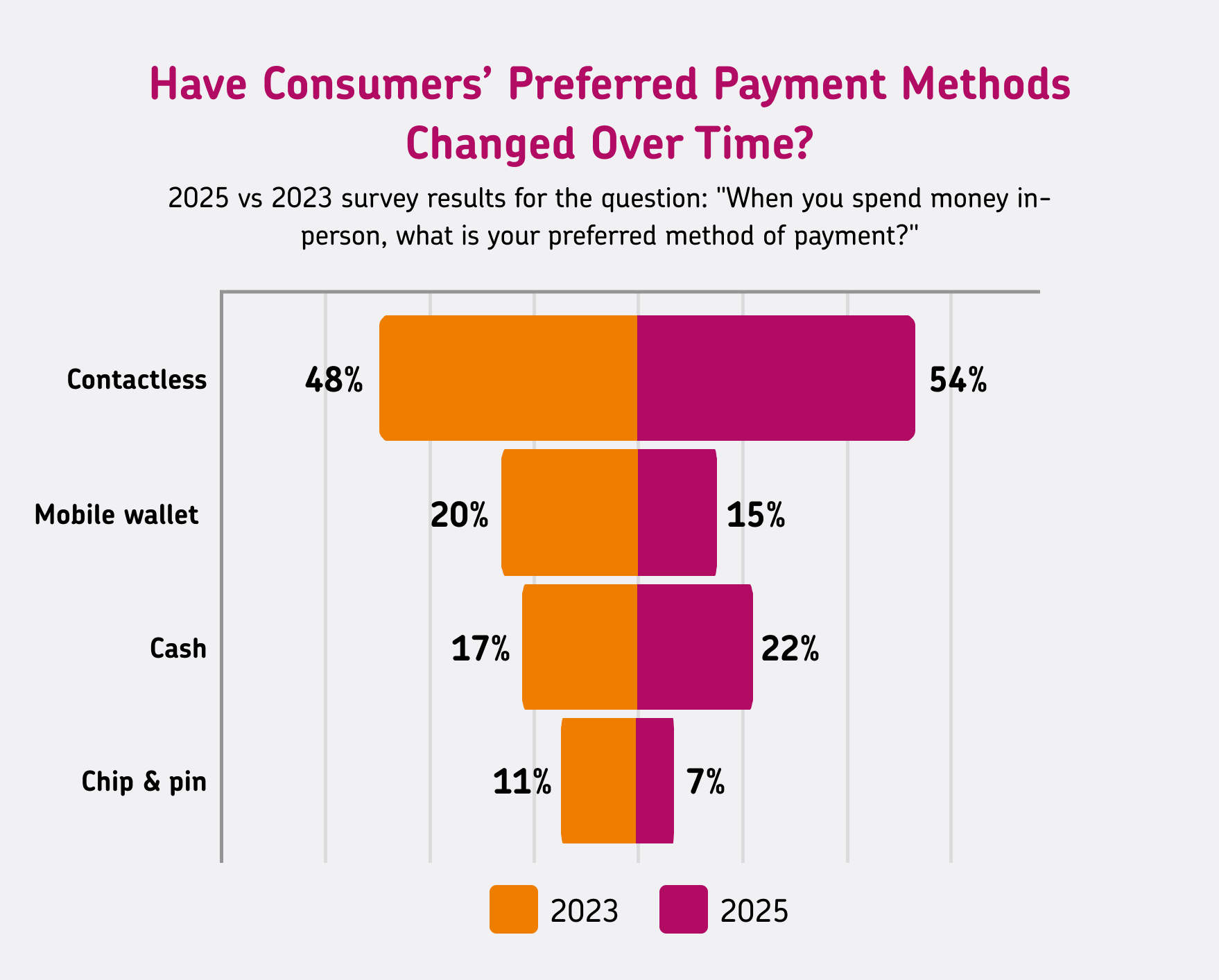

Have consumers' payment preferences changed over time?

So, what’s really shifted since we last asked shoppers how they prefer to pay in person? The answer is that payment habits are still evolving — but not always in the way you’d expect.

Contactless remains on top, and its popularity has grown even more. Compared to 2023, consumer preference for contactless has increased by 14%, proving that shoppers still love the speed and ease of tapping to pay.

Meanwhile, cash has made a surprising comeback. In-store preference for cash has grown by 26% year on year, pushing it ahead of mobile wallets to become the second most popular way to pay. On the other hand, mobile wallets have dipped in popularity for in-store payments, down by a quarter compared to 2023 (26%).

With such a customer expectation for convenience, it’s unsurprising that chip and PIN declined by 37% year on year, marking the biggest decrease across all in-store methods.

Do age and gender affect in-store payment preference?

Payment habits aren’t the same for everyone, and our survey findings show that age and gender can make a big difference to what shoppers choose at the till.

Contactless is still the top pick across every age group, but the 25–34s were the least likely to name it as their favourite, at just 42%. By comparison, over half of over-55s were more likely to stick with contactless (62%).

When it comes to cash, the same two groups — 25–34s and over-55s — are the most likely to use it for in-store purchases (23%). Meanwhile, younger shoppers aged 18–24 are still the biggest users of mobile wallets when paying in person.

Gender also plays a part: women remain slightly more likely to choose contactless as their favourite method (57% against 52% for men), and 23% more likely to choose mobile wallets (13% against 16% for men).

Men are 32% more likely than women to pick cash (25% against 19% for women), and this gap has widened since 2023, when there was almost no difference.

Why is contactless so popular in 2025?

It’s no surprise that speed and ease are still the main reasons why shoppers reach for contactless.

When asked the reasons why contactless is their favourite in-store payment option, the majority (87%) said they did so because it’s simply the most convenient option, and 44% said it's because it offers a faster transaction time. Wide acceptance also plays a part, with 31% saying they prefer contactless because they know they can use it almost anywhere.

Are consumers still carrying and using cash in 2025?

Despite predictions of a cashless society, cash has actually grown in popularity over the last two years, proving it still plays a key role on the UK high street.

More than half of shoppers (56%) say they still carry cash day-to-day, with another 41% doing so occasionally, leaving only 3% who never use it at all.

When asked why they prefer paying with cash, 61% said they do so because it’s convenient, while 41% said it helps them stick to a budget. 37% feel that paying with notes and coins is faster in certain situations, and 29% said they see cash as the most secure option.

A dig into cash usage by age group also revealed that 66% of over-55s always have cash on them, but even half of 18–24s say they carry it at least some of the time (50%).

Rona Warne, Head of Marketing UK&I at Global Payments (takepayments is now a Global Payments company), addresses the shift: “Seeing security concerns pop up for cash users — especially among younger shoppers — is a big reminder for small businesses to show how safe their card and digital payments are. Simple steps like displaying trusted payment logos at the till, keeping systems up to date, and using secure card machines can all help to build customer trust and reassurance.”

Would consumers buy from a shop that doesn’t offer digital payment methods?

In 2025, having flexible payment options isn’t just a nice-to-have; it could be the difference between making a sale or losing it altogether.

Our survey found that while most shoppers would still buy from a business that only accepts cash, more than half (52%) say it would be inconvenient. That’s up nearly 20% from 2023 (33%), highlighting that expectations for digital payment options are growing every year.

While more people want digital payment options, only 6% said they wouldn’t buy from a store if they didn’t offer them at all, down 8% from 2023 (13%).

Younger shoppers are the least willing to deal with cash-only businesses: 26% more 18–24s now say they’d find it inconvenient compared to two years ago. On the other hand, only 2% of 25–34s said it would be a hassle, showing that attitudes can vary widely even between neighbouring age groups.

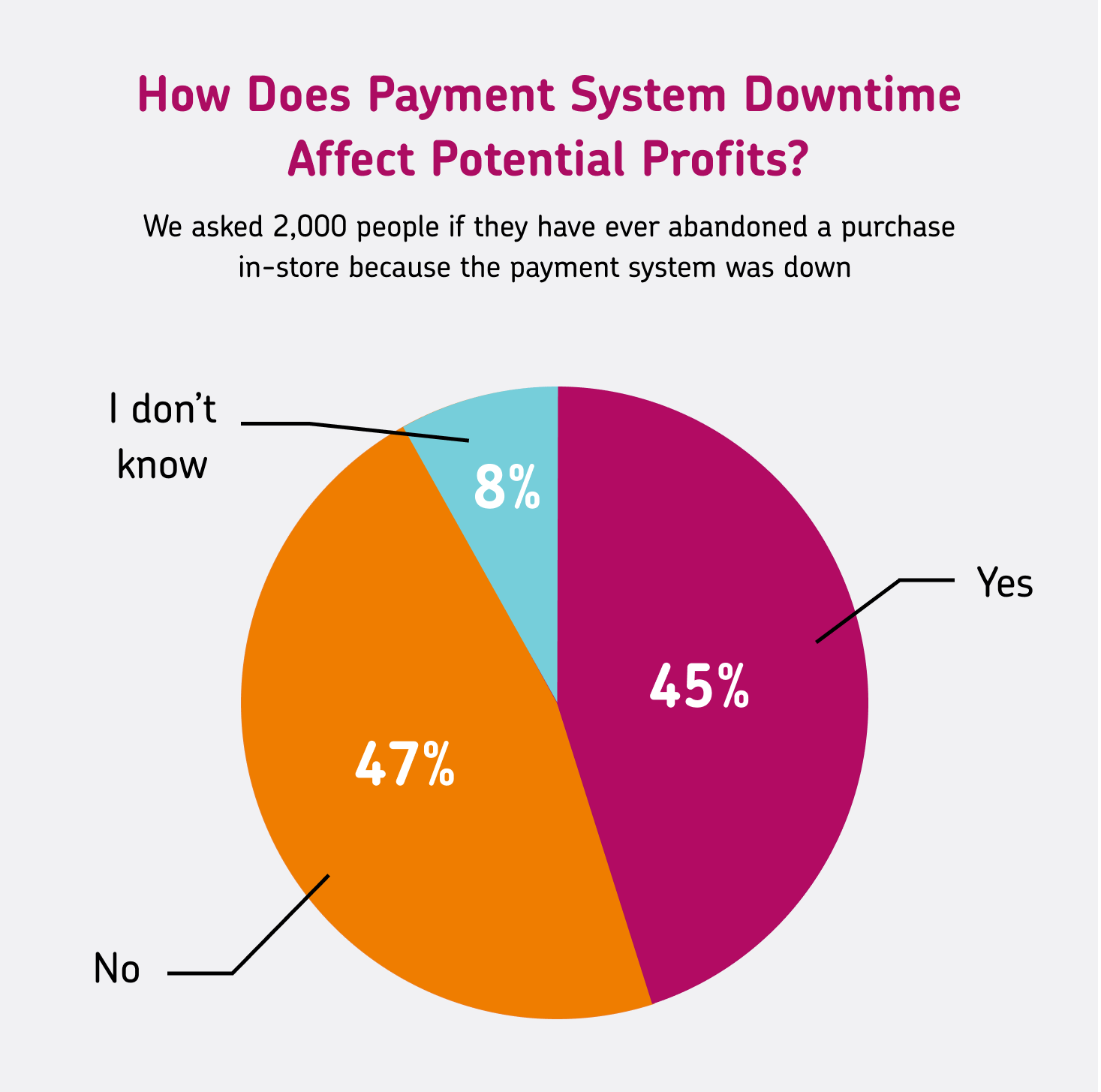

How do consumers deal with payment system downtime?

Even if you have a top-of-the-range payment system, it can all fall apart if it goes down, and shoppers won’t always wait around.

45% of people say they’ve abandoned an in-store purchase because the payment system wasn’t working.

The main reason? One in three (34%) said they didn’t have cash and simply couldn’t pay any other way.

Others said switching to cash from card was too time-consuming (28%) or that a technical failure made them doubt the safety of the shop’s systems altogether (28%).

For small businesses, it’s a clear warning that even a short payment outage can damage sales and your reputation.

“Regular, local testing of your payment systems is more critical than ever, especially before rolling out any updates. We saw major supermarkets like Sainsbury’s and Asda suffer nationwide payment outages in 2024 after system failures left shoppers unable to pay by card, and it shows just how quickly technical issues can bring sales to a grinding halt. Small businesses can’t always absorb that kind of disruption, so they should consider piloting any software or terminal updates in a local environment before full rollout, as this can reduce the chance of widespread system failure,” says John Clark, Product Manager at takepayments.

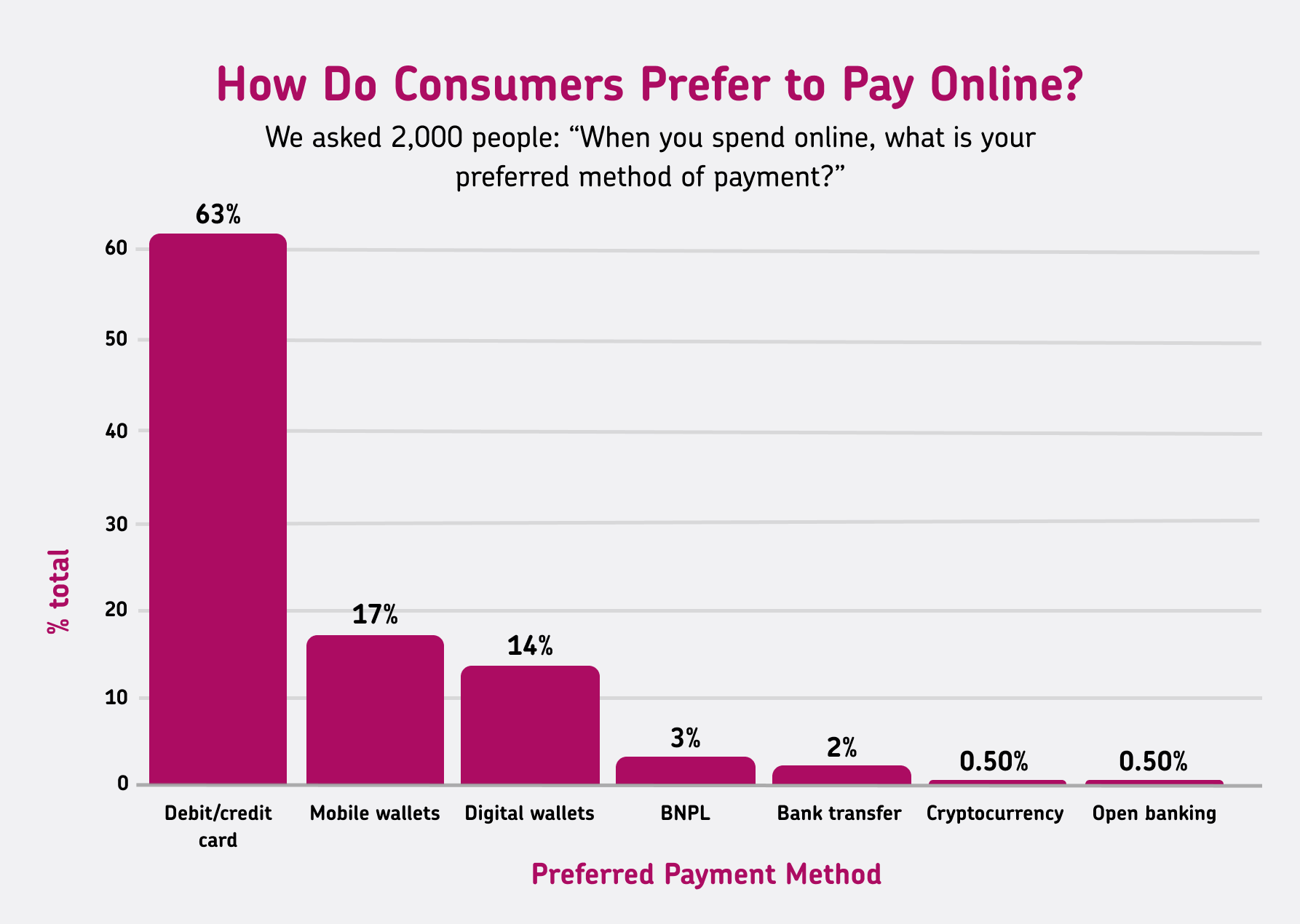

How do consumers prefer to pay online?

Debit and credit cards are still the clear favourites for UK shoppers buying online. 63% say it’s their go-to payment method, showing that trusted, familiar ways to pay continue to dominate even as new options emerge.

Mobile and digital wallets are gaining ground, too, especially among younger shoppers. 17% say they prefer mobile wallets like Apple Pay when buying online, while 14% choose digital wallets like PayPal or Amazon Pay.

Interestingly, Buy Now Pay Later (BNPL) continues to lag behind with just 3% of people saying it’s their preferred online payment method.

When asked why, 65% said they picked their favourite online payment method because it’s quick and straightforward. A third (34%) value fast transaction times, and 31% like to know their chosen method is widely accepted. For debit and credit cards, 7 in 10 shoppers say they stick with them because they know they’re accepted everywhere (69%).

Does age or gender affect online payment preference?

Over-55s are the most likely to stick with debit and credit cards when buying online, with more than three-quarters (77%) saying it’s their top choice. At the other end of the scale, 18–24s are leading the charge for mobile wallets: 42% of this age group now prefer them when shopping online, even ahead of cards (39%).

Younger shoppers also show more interest in digital wallets like PayPal, while those aged 25-54 lean towards debit and credit cards as their favourite payment method. Those in the 25-34 age group were most likely to choose BNPL.

Gender makes a difference, too, though not as strongly as age. Men show a higher preference for debit and credit cards (67% compared to 58% for women), while women are slightly more likely to choose mobile (19% compared to 14%) or digital wallets (15% compared to 13%).

Interestingly, women are also more likely than men to use Buy Now Pay Later when shopping online (4% vs. 2%).

“These figures show there’s still a clear divide in how different age groups approach paying online. While younger shoppers are driving the growth of mobile wallets, older generations still prefer traditional debit and credit cards, which means businesses need to cover both bases to keep everyone happy at checkout.”

“It’s also interesting to see that women are more open to using a wider mix of digital payment methods, from mobile and digital wallets to BNPL, while men seem to prefer a more traditional option. Offering flexible payment choices is a simple way for small businesses to meet these varied expectations and make sure no sale is left behind,” says Rona.

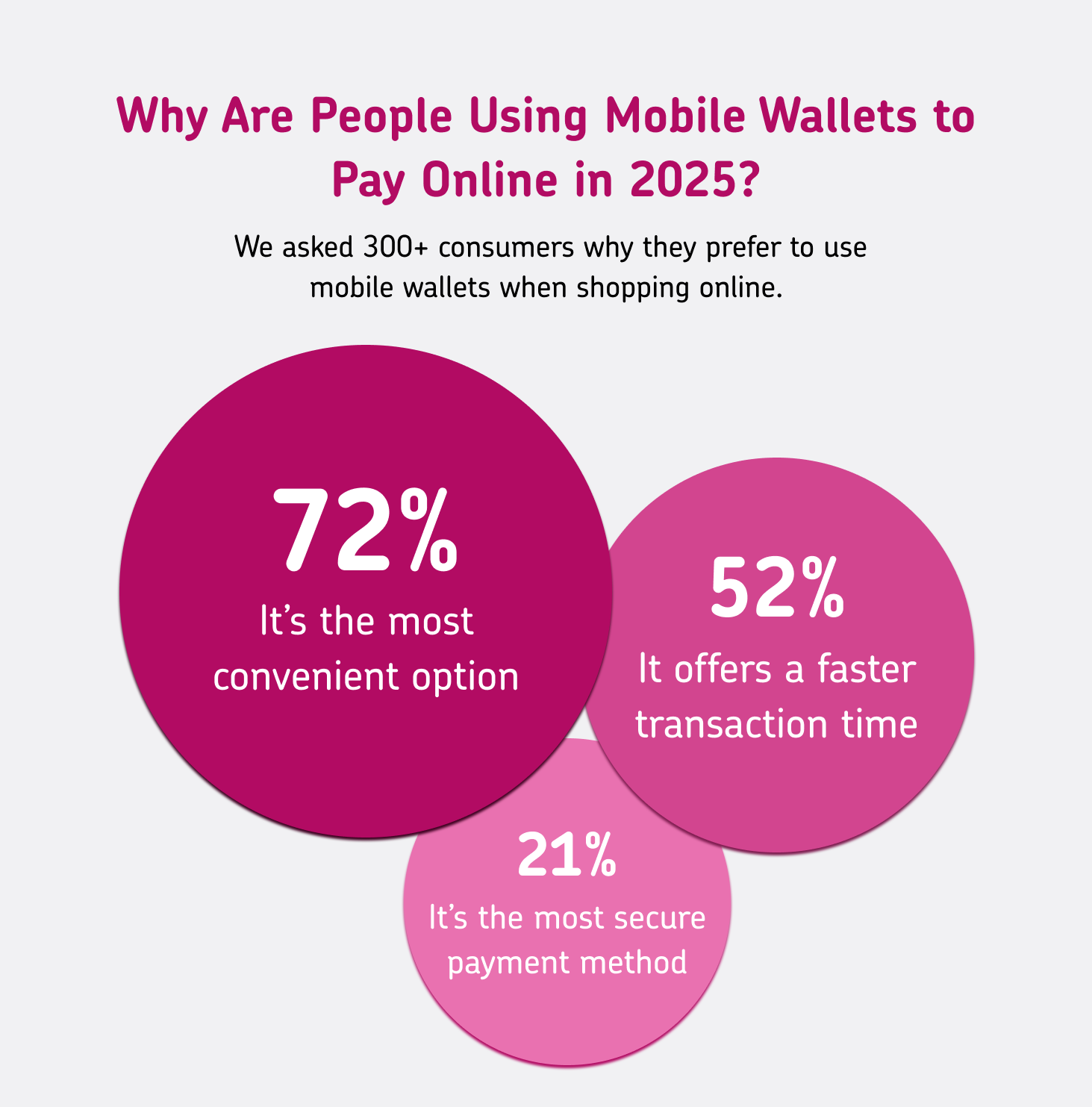

Why are people using mobile wallets to shop online in 2025?

Mobile wallets are now an everyday part of online shopping, and the reasons behind what's keeping this method popular are clear. For many, it all comes down to speed and simplicity.

72% of those who prefer mobile wallets say they use them because they are the most convenient option. 52% value faster transaction times, while one in five (21%) choose mobile wallets because they see them as the safest way to pay online.

This shows small businesses how important it is to make mobile payments quick, smooth and trustworthy. Shoppers now expect a frictionless checkout experience and may look elsewhere if it’s not up to scratch.

Rona explains, ”It’s clear that speed and convenience still win over security for many online shoppers. People want a checkout that works quickly with as little friction as possible, which is why mobile wallets keep growing in popularity. But just as important is giving your customers a choice. Not everyone trusts or wants to use the same payment method every time.”

Do mobile and digital wallets affect online shop loyalty?

The right payment options can make or break a sale, and our survey shows just how much shoppers value having mobile and digital wallets at checkout.

Around 15% of shoppers say they wouldn’t complete a purchase if their preferred mobile or digital wallet option wasn’t available. While nearly half (46%) have no preference, around one in three shoppers (34%) say they would still buy from an online store that didn’t accept mobile or digital wallets, but it would be an inconvenience.

Shoppers under 45 are far more likely to feel inconvenienced by the lack of wallet options, while those over 45 are generally more flexible about how they pay online. For example, almost half of shoppers aged 35–44 said they’d find it frustrating not to be able to use a mobile or digital wallet, compared to just a third of shoppers under 35.

“Small businesses can stay one step ahead by making sure their checkout process accepts cards, mobile wallets, and digital wallets like PayPal. Regularly reviewing your payment setup, testing it on different devices, and keeping it simple can help you turn browsers into buyers, and stop abandoned baskets before they happen,” says Rona.

What security measures do consumers look for when shopping online?

We know that security is one of the top priorities for shoppers when it comes to online payments, so let’s dig into what factors help build trust.

The majority (72%) say they look for the Verified by Visa or Mastercard SecureCode symbol, showing that customers want visible reassurance that their payment details are safe.

Other common security measures that shoppers value include secure payment gateways (40%), which you can spot via the padlock symbol and “https” in a webpage’s URL. 36% also prefer two-factor authentication (e.g. OTPs sent to their phone), while 25% of shoppers expect strong password requirements.

“Consumers are more informed than many businesses might realise when it comes to online payment security, and all the IT outages in 2024 have only made consumers even more aware of where they’re tapping, swiping, or entering their card details. For small businesses, displaying trusted security symbols and ensuring the checkout process uses secure payment gateways can help build customer trust, but they should also clearly communicate this to customers,” John explains.

Learn more about card payment security measures here and how your business can implement them.

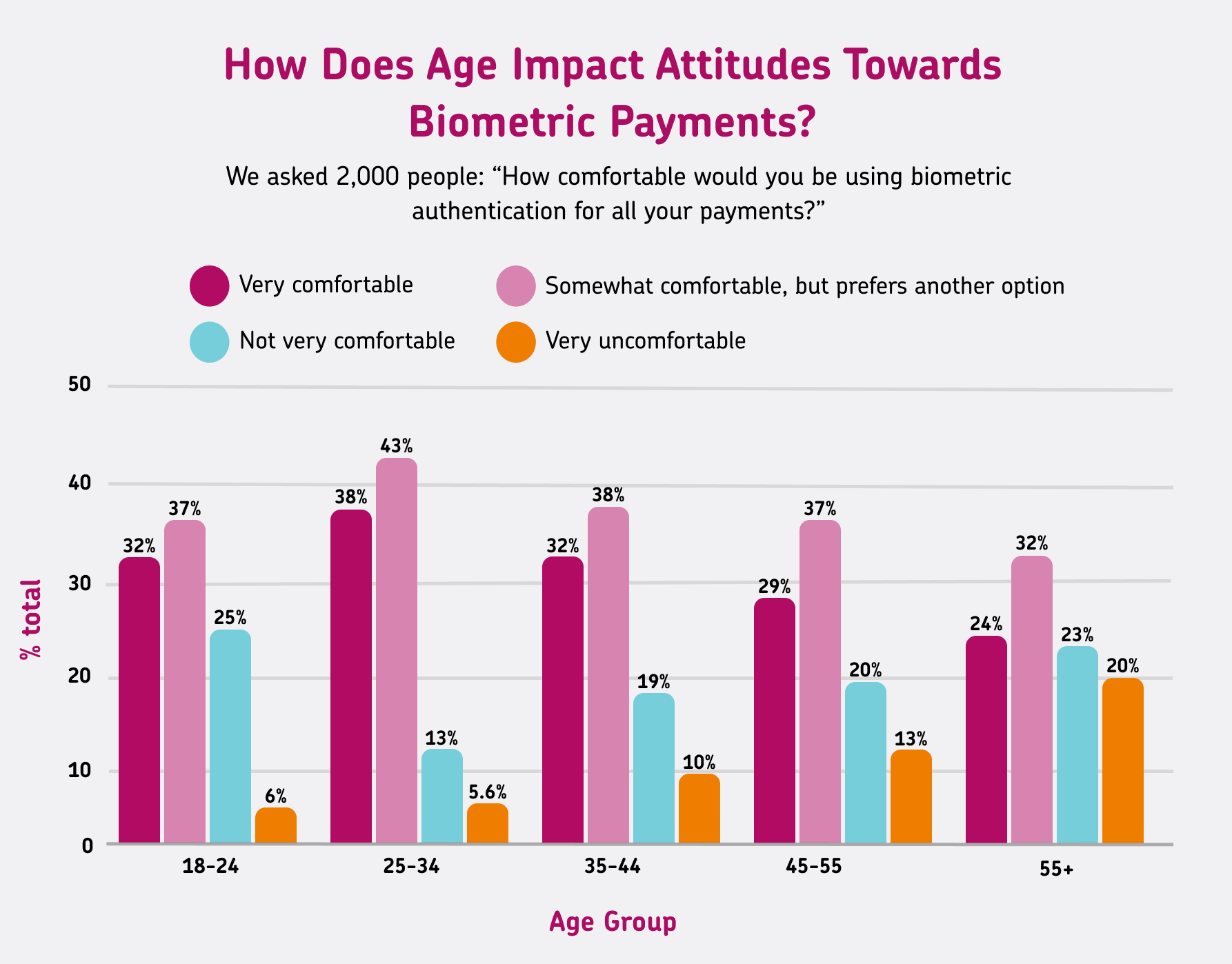

How comfortable are consumers with biometric payments?

The adoption of biometric payments, such as facial recognition and fingerprint scanning, is one of the payment trends that is expected to increase in the coming years, but not all consumers are on board yet.

Around two-thirds (67%) of people say they would feel somewhat comfortable using biometric payments as their sole method for authorising transactions, and 2 in 5 said they’d be comfortable but would prefer another option. However, a third (32%) still feel uneasy about the idea, especially when it comes to giving up their personal data.

Comfort levels vary by age group; 25-34s were the most open to biometric payments with 81% of them stating they were comfortable to some extent. On the other hand, 43% of over-55s said they were apprehensive, and 20% felt very uncomfortable.

What aspect of shopping online frustrates consumers the most?

Despite the growing convenience of online shopping, there are still plenty of pain points that leave customers frustrated at checkout.

The most common grievance for shoppers is having to input card details, with nearly 30% saying it’s the most annoying part of online payments. For many, entering a card number, expiry date, and CVV for every purchase feels like an unnecessary hassle, especially with the speed and convenience of mobile wallets and digital payment methods.

Other frustrations include having to create an account with a business before making a purchase (20%) and dealing with extra security checks like one-time passcodes or answering security questions (19%).

How do consumers feel about open banking when shopping online?

Open banking, technology that allows consumers to make payments directly from their banking app without entering card details, is slowly gaining traction.

Just over half (52%) of shoppers say they’d feel comfortable using open banking to make payments when shopping online, while around 23% say they wouldn’t feel comfortable at all.

For those who are uncomfortable with open banking, the most common reasons were concerns over security, with 38% citing fears of hacking or data breaches. Another 29% were uneasy about sharing their bank details with third parties.

On the other hand, those who feel comfortable with open banking said the biggest reason is that they trust in the method's security, with 46% citing this as a primary factor. 31% said they simply find it quicker and easier than entering card details.

Younger shoppers (18–24s) are the most open, with only 16% expressing discomfort. However, for shoppers over 55, nearly a third (33%) are still not ready to embrace this payment method.

“While open banking is gaining traction, especially in the UK, where there are an estimated 7 million users, there is still a long way to go before it becomes a fully trusted payment method for the majority of consumers,” says Rona.

“Even though younger shoppers are more likely to embrace it, a significant portion of consumers remain cautious, particularly due to security concerns like data breaches or sharing sensitive banking details with third parties. For small businesses, there’s an opportunity to lead the charge in educating your customers about the safety and benefits of open banking, but also to be mindful of customer hesitancy.”

Read up on open banking and other common types of payment methods here.

The key takeaways for small businesses

John outlines what small businesses should prioritise for payments in the future:

“The new data highlights the growing importance of offering multiple payment methods to meet customers' evolving expectations. While mobile wallets and digital payment options are seeing faster and widespread adoption, traditional methods like cash and card payments are still crucial for many shoppers. This also makes them essential for businesses, as failing to provide a variety of payment options could result in lost sales, as customers may turn to other brands that offer more flexibility.

For businesses looking to optimise their payment systems, here are our key takeaways:

1. Providing a variety of payment options is essential to meet customer expectations

Customers expect flexibility — online and in-store. In our survey, while contactless transactions were the clear favourite, respondents named a range of other payment options as their preferred method.

By providing a mix of traditional and digital options, you can meet the needs of all shoppers and make sure that no one gets left out. This increases convenience and reduces the risk of abandoned purchases.

2. Displaying visible security measures builds trust and confidence in your business

Consumers are more aware of potential security risks than you might think, so making sure your payment systems are secure is crucial. Displaying well-recognised security symbols like Verified by Visa or Mastercard SecureCode and using trusted payment gateways can help reassure customers that their payments are secure. We also discovered that payment system downtime significantly impacts how customers view your security level. Regular payment system testing and a backup plan can prevent any unexpected disruptions whilst also protecting your sales and reputation.

3. Streamlining the checkout process can significantly improve the customer experience

Security protocols like entering a one-time passcode might be time-consuming, but they’re non-negotiable for keeping customer data safe. However, there are other barriers that businesses can do something about.

16% of our survey respondents said that technical issues like slow-loading pages are their biggest frustration when shopping online, so businesses should find ways to reduce friction and create a speedier checkout flow. Offering guest checkout, allowing customers to save their payment methods for future purchases, and implementing one-click payment options can simplify the process and encourage repeat business.

4. Educating your customers about new payment methods can help build trust and increase adoption

While open banking is still in its early adoption stage, providing information on how it works and how secure it is can help build trust among your customers.

It’s all about balance, though, so don’t forget about more traditional methods that a large portion of consumers still rely on. By offering open banking alongside other options, you can appeal to younger, tech-savvy consumers who value speed and convenience.

5. Payment system downtime could halve profits

Payment system failures can lead to significant losses, with nearly half of consumers (45%) saying they’d abandon a purchase if the payment system goes down.

To mitigate this risk, businesses should regularly test their payment systems, ensure they have backup options, and keep customers informed if any issues arise to avoid disruptions and potential loss of revenue.”

Methodology

takepayments conducted a survey of 2,000 UK residents aged 16-86 in June 2025. The survey contained 15 multiple-choice questions based on their preferred payment methods in-store and online. The results were broken down by gender and age, and compared to the results of a similar survey of 1,056 UK residents from 2023.

The study was conducted using the survey platform Pollfish.

More insights from takepayments

Want more original statistics about UK businesses and consumer behaviours? Check out these other data reports and tools from our team: